Buy now, pay later tools have slipped quietly into the travel world. On many airline, hotel and online travel agency checkouts, PayPal now appears with a tempting Pay Later button that lets you split your trip into smaller payments instead of paying everything upfront. For cash‑strapped travelers, that can look like the perfect solution. Before you use PayPal Pay Later for your next flight to Lisbon or last‑minute hotel in New York, though, it is worth understanding exactly how it works, where the risks lie, and how to protect yourself if plans change.

Get the latest updates straight to your inbox!

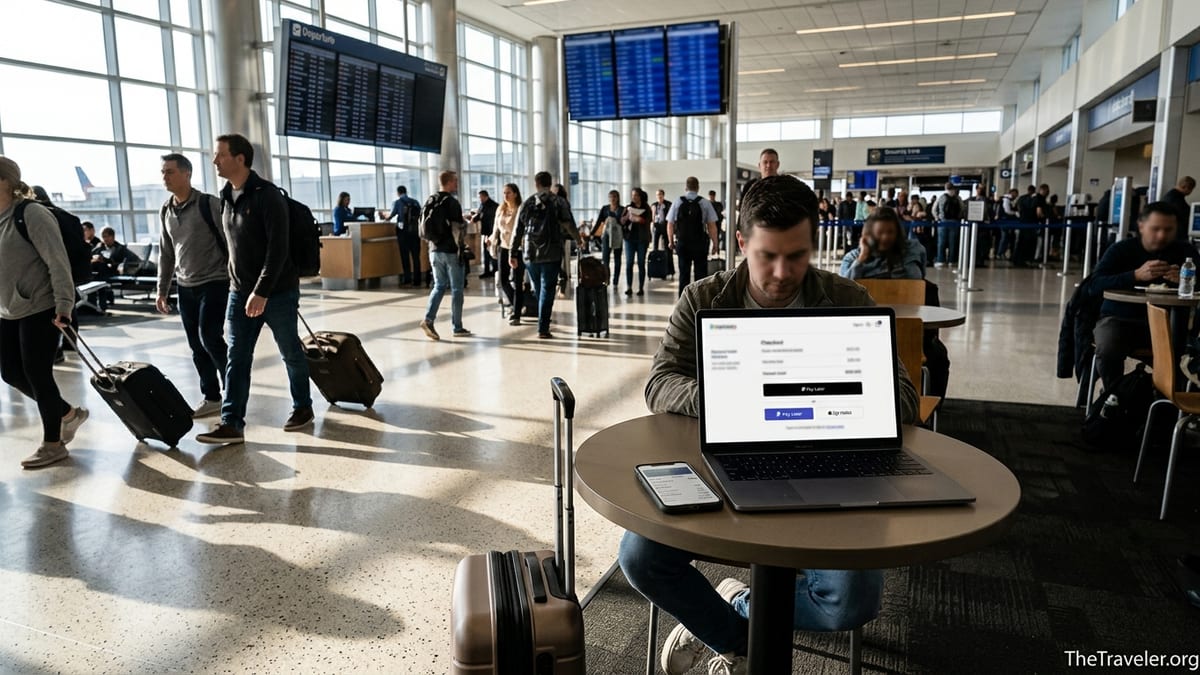

1. How PayPal Pay Later Actually Works for Travel Bookings

PayPal Pay Later is PayPal’s buy now, pay later option, most commonly offered as Pay in 4 and Pay Monthly in the United States. When you book travel with a participating airline, hotel, or online travel agency and select PayPal at checkout, you may see a choice to divide your purchase into four interest‑free payments over roughly six weeks (Pay in 4) or into longer monthly installments with interest (Pay Monthly). PayPal promotes this feature directly for travel, pointing out that you can use it for flights, hotels, car rentals and vacation packages when the merchant supports PayPal at checkout.

In practice, a typical Pay in 4 plan for a $600 round‑trip flight to Mexico City would charge you $150 at checkout, then three more $150 payments every two weeks, all automatically taken from your linked debit card, bank account or other funding source. Pay Monthly works more like a small installment loan. For example, PayPal has illustrated that a $600 purchase financed over six months at an annual percentage rate in the mid‑20s results in monthly payments a little above $100, depending on the exact APR and term. The key is that you receive your ticket or hotel booking right away, while your obligation to PayPal stretches out over time.

Behind the scenes, PayPal usually pays the travel merchant the full amount shortly after you complete your transaction and then collects your installments. Approval is not guaranteed and is decided case by case. PayPal runs a soft credit check for each application, which does not by itself show up as a hard inquiry on your traditional credit report. However, it still reviews your credit profile and your prior Pay Later behavior, so previous missed BNPL payments or heavy use of other buy now, pay later products can affect whether you are approved.

For travelers, the big appeal is being able to lock in a flight or hotel price now, especially for peak periods like summer in Europe or New Year’s Eve in Las Vegas, even if payday is a couple of weeks away. That convenience is real, but it comes with strings that are easy to underestimate when you are focused on snagging a deal before a fare jumps.

2. Approvals, Limits, and Why Your Pay Later Option May Disappear

One important thing travelers discover only at checkout is that PayPal decides in real time whether to offer Pay Later for a specific purchase. You might see Pay in 4 one day and then find it missing the next, even with the same airline. Approval can depend on the trip cost, your recent PayPal activity and your broader credit profile. Travelers on forums regularly describe situations where they used Pay in 4 successfully for several hotel stays, then suddenly received a “PayPal not available at this time” error when trying to buy a flight, despite having never missed a payment.

There is no published universal spending limit, but Pay in 4 is typically geared toward smaller to mid‑sized purchases. A $300 budget hotel stay in Chicago is more likely to qualify than a $2,000 business‑class ticket to Tokyo. Pay Monthly is designed for larger purchases and may show up instead when your cart total is higher. Even then, PayPal may still decline a booking that pushes your overall exposure too far, especially if you already have several active Pay Later plans, a pattern regulators have flagged across the BNPL market.

Another surprise is that PayPal generally wants to see that your underlying funding source can cover the full amount of the trip at the time of booking, even though it only charges you the first installment upfront. Travelers who try to use Pay in 4 with a nearly empty checking account sometimes find the transaction fails or remains in a “pending” state. Picture a traveler booking a $450 JetBlue ticket using Pay in 4 with just $200 in their bank account. PayPal might place a temporary authorization hold for the full $450 against the funding source as part of risk checks, which could then bounce or tie up funds needed for other expenses, even though only $112.50 is due that day.

A final point: approvals are transaction specific. Using Pay in 4 for a $120 airport hotel in Denver does not guarantee Pay in 4 will be offered, or approved, for a $600 holiday rental the next day. If using Pay Later is central to your trip budget, be prepared for the possibility that it will not be available at the exact moment you want to book, and have a backup payment strategy.

3. What Happens If Your Flight or Hotel Is Changed, Canceled, or Refunded

Travel rarely goes exactly to plan, and this is where PayPal Pay Later can get complicated. When you pay directly with a credit card and your flight is canceled, the airline typically issues a refund back to that card. With Pay Later, the airline or hotel refunds PayPal, and PayPal then has to apply that refund to your installment plan. In many straightforward cases, the plan is adjusted within a few days: upcoming payments are reduced or canceled, and if you already paid more than the final amount, PayPal returns the difference.

However, consumer advocates and regulators have documented a steady stream of complaints about refunds on buy now, pay later travel purchases. In some scenarios, the airline insists it has sent the money back, while the BNPL provider says it has not received it or is processing it, leaving travelers in limbo. For example, a traveler who books a $1,000 all‑inclusive package through an online agency and pays via Pay Monthly might see the trip canceled due to an overbooked hotel. The agency claims it has refunded PayPal, but the traveler is still watching $90 auto‑debited every month while waiting for the adjustment to show up.

Refunds can be slower when the travel provider issues credits rather than cash. Many low‑cost airlines respond to schedule changes with vouchers or travel credits instead of cash refunds. If your $300 Los Angeles to Honolulu ticket becomes a voucher in the airline’s system, PayPal may not automatically know how to treat that on the installment plan, particularly if the voucher value is tied to rebooking directly with the airline. In those cases, you can end up making payments on a loan even though your original flight no longer exists and you are still negotiating with the airline for a usable credit.

Non‑refundable rates add another layer of risk. Because Pay Later loans are set up at checkout, PayPal normally keeps charging the installments even if you change your mind and the hotel or airline refuses a refund. A traveler who impulsively grabs a non‑refundable, prepaid resort stay in Cancun for $700 using Pay in 4, then realizes a day later that their passport has expired, may be stuck paying all four installments whether or not they can travel. PayPal is not the one promising flexibility; it only reflects the merchant’s rules.

4. Fees, Credit Impact, and How Pay Later Fits Into Your Financial Life

PayPal currently markets Pay in 4 in the U.S. as having no interest and no late fees, while Pay Monthly charges interest but no explicit late fees. That sounds straightforward, but travelers should think carefully about the broader cost. While an interest‑free plan on a $300 city‑break hotel night in Boston truly does not add extra finance charges if you pay on time, Pay Monthly for a $2,000 family trip to Orlando can look very different when stretched over 12 or 24 months at a double‑digit APR.

Regulators like the Consumer Financial Protection Bureau and the Federal Reserve have noted that heavy BNPL users tend to carry more credit card and other unsecured debt than average and may be more likely to overextend themselves. For a traveler already juggling a car payment, student loans and a couple of revolving credit card balances, adding several concurrent Pay Later plans for flights, hotels and concert tickets can make it harder to see their true monthly obligations. The fact that payments are smaller and scattered over weeks or months can hide the cumulative impact on your budget.

On the credit‑reporting side, PayPal’s pay‑in‑four style loans have historically not been reported in the same way as traditional credit cards or personal loans, although that landscape is evolving as credit bureaus and BNPL providers experiment with new models. A soft credit check for approval does not itself hurt your score, but missed payments can have consequences. PayPal reserves the right to attempt collection from your backup funding sources if a scheduled debit fails, and delinquent accounts may eventually be sent to collections, which can damage your credit history.

From a practical standpoint, travelers should treat Pay Later just like any other form of credit. If you would be nervous putting a $1,000 Greece flight on a high‑APR card and carrying it for months, be just as cautious about agreeing to a year‑long Pay Monthly plan for the same ticket, even if the checkout screen emphasizes the size of the monthly payment instead of the interest rate.

5. Disputes, Chargebacks, and Your Rights as a Traveler

One of the most important developments for U.S. consumers is that regulators have moved to clarify that key credit card protections apply to many buy now, pay later loans, including those from PayPal. That includes the right to dispute charges when the service is not delivered or is misrepresented. For travel, this might cover situations like an airline that refuses to honor a ticket, a hotel that turns out to be closed on arrival, or a tour operator that goes out of business before your departure.

In practice, though, asserting these rights can be more complicated with Pay Later than with a traditional credit card. Instead of calling your card issuer and initiating a straightforward chargeback, you are dealing with PayPal as an intermediary, and your complaint may involve three parties: you, the travel merchant and PayPal. Travelers have reported cases where the airline insists that any dispute must go through PayPal, while PayPal’s customer service requires extensive documentation from the airline to pause or reverse installment payments. That back‑and‑forth can be especially painful when the disputed amount is still being debited from your account every two weeks.

Imagine you book a $900 multi‑city itinerary through an online travel agency using Pay in 4. The first leg is canceled shortly before departure, and the agency fails to secure an adequate alternative. You cancel the whole trip and request a refund, but weeks later you are still paying the third and fourth installments while the agency and PayPal sort out who owes what. Under current interpretations, you have a right to contest the charges and seek a pause in payments, but you will need to be proactive: keep copies of all emails, cancellation notices, and refund confirmations; open a dispute promptly in your PayPal account; and be prepared to escalate if responses are slow or confusing.

One practical downside compared with paying directly by credit card is that some credit card issuers are very experienced at handling travel disputes and often swing into action quickly when you report a problem. With Pay Later, you are relying on PayPal’s dispute process and timeframes instead of your card issuer’s, which may feel less familiar and less predictable if you have never used it before.

6. Planning Around Payments, Currencies, and Travel Timing

Using PayPal Pay Later for travel is not just about being approved at checkout. You also have to live with the payment schedule once you are on the road. Pay in 4 splits your purchase into four payments over roughly six weeks. That means a flight you book in early August for a September trip to Paris will still be generating installments while you are away. If your bank balance tends to dip while you are traveling, those automatic debits can collide with hotel incidentals, restaurant charges and local transportation costs.

Travelers should sit down and map the actual calendar dates of their installments. Suppose you use Pay in 4 to pay $800 for a pair of economy flights from New York to Lisbon, with $200 due at checkout on June 10, then three more $200 payments on June 24, July 8 and July 22. If your trip runs from July 1 to July 14, two of those payments fall while you are abroad. Being hit with an unexpected overdraft fee at home because a Pay Later installment posted the same day you picked up a rental car in Portugal can erase any benefit of spreading out the airfare.

Currencies matter too. Many U.S. travelers book foreign airlines or overseas hotels priced in euros, pounds or other currencies through websites that accept PayPal. In those cases, PayPal handles currency conversion, and its exchange rate may include a margin above the interbank rate. Pay Later does not exempt you from those conversion costs. So if you use Pay in 4 to reserve a €600 boutique hotel in Paris directly on the hotel’s site, your total in dollars may shift slightly between authorization and settlement depending on how the merchant processes the transaction and how PayPal applies its rates. While those movements are usually modest, they can complicate budgeting if you are counting every dollar.

Another nuance is that Pay Later works only where merchants accept PayPal and where PayPal chooses to offer the option. Many smaller guesthouses, rural lodges, or niche tour operators around the world still prefer direct credit card payments or bank transfers and never present a PayPal button at checkout. Even among major U.S. airlines, availability varies by sales channel. A carrier might support PayPal Pay Later on its website but not in its mobile app, or vice versa, and availability can be switched on and off during system changes or promotions. It is wise not to assume that you will be able to use Pay Later for every part of a complex itinerary.

7. When Using PayPal Pay Later for Travel Might Make Sense

Despite the risks, there are situations where PayPal Pay Later can be a useful tool for travelers who plan carefully. One example is bridging a very short‑term cash gap for a necessary, time‑sensitive purchase. If you need to fly home next week for a family emergency and can comfortably cover the full cost within the next month but do not have enough in your checking account today, an interest‑free Pay in 4 plan on a $400 ticket could be a reasonable alternative to running up a balance on a high‑APR card, provided you are certain the installments will clear without strain.

Another scenario is managing a fixed, predictable trip cost in a tight but stable budget. A traveler booking a $360 set of train passes across Japan six weeks before departure, who receives paychecks every two weeks and tracks all commitments in a spreadsheet or budgeting app, might find Pay in 4 a convenient way to match payments to paydays. Here, the risk of overextension is lower because the traveler has mapped out each installment and left a cushion for other expenses.

Some travelers also value the separation between day‑to‑day card use and a dedicated Pay Later plan. By putting a $700 safari deposit or a $500 domestic flight for an upcoming conference on Pay Later, they keep their main credit card limit open for on‑trip spending and emergencies. This can make sense if they already pay that card in full each month and use Pay Later sparingly as a specific planning tool rather than a default payment method.

The key is intentionality. PayPal Pay Later is most dangerous when used impulsively, such as clicking Pay in 4 on a $1,200 last‑minute luxury hotel upgrade at the end of a long search session, or stacking multiple plans for flights, concert tickets and festival passes without tallying the final monthly hit. If you treat it like any other loan and build it into a realistic travel budget, it can be part of a responsible strategy to spread out costs, but it is rarely a magic solution.

The Takeaway

PayPal Pay Later has brought the buy now, pay later trend firmly into the travel world, offering an easy way to split the cost of flights, hotels and packages into smaller bites. Beneath that convenience lies a complex mix of approvals, refund rules, regulatory protections and budgeting challenges that can trip up unwary travelers. From surprise denials at checkout and pending authorizations on your bank account to slow refunds when itineraries change, the details matter more than the marketing slogans.

Before you rely on Pay Later to make a dream trip possible, take the time to read both PayPal’s terms and your airline or hotel’s fare rules, map out the exact payment schedule across your travel dates, and consider how another installment plan fits with your existing debt. In some cases, paying in full with a credit card that offers strong travel protections, or simply waiting to book until you have the cash, will be safer. Used carefully, PayPal Pay Later can be one more tool in a traveler’s toolkit. Used casually, it can turn a relaxing getaway into months of financial catch‑up long after your suitcase is unpacked.

FAQ

Q1. Can I use PayPal Pay Later for any flight or hotel booking?

Not always. You can only use PayPal Pay Later where the merchant offers PayPal at checkout and where PayPal chooses to display Pay in 4 or Pay Monthly for that specific transaction. Some airlines, hotels and online travel agencies support it on their websites but not in their apps, and availability can change over time.

Q2. Does PayPal Pay Later charge interest or fees on travel purchases?

PayPal’s Pay in 4 plan is typically interest free and has no explicit late fees if you pay on time, while Pay Monthly charges interest over a longer term. However, you still face any applicable currency conversion costs and normal bank fees, and missing payments can trigger collection efforts or damage your credit profile.

Q3. Will using PayPal Pay Later for a trip affect my credit score?

Applying for Pay Later usually involves a soft credit check that does not appear as a traditional hard inquiry. However, if you repeatedly miss payments and your account becomes seriously delinquent, it may ultimately be sent to collections, which can harm your credit history just like other unpaid debts.

Q4. What happens if my flight booked with PayPal Pay Later is canceled?

If your airline or travel agency issues a cash refund, it normally goes back to PayPal, which then adjusts your Pay Later plan by canceling future installments or refunding overpayments. In practice, this process can be slow or confusing, so you should monitor your PayPal account, keep documentation from the airline and contact PayPal promptly if installments continue after a refund is promised.

Q5. Can I change or reschedule a non‑refundable trip paid with PayPal Pay Later?

Using Pay Later does not make a non‑refundable booking refundable. If the airline or hotel will not issue a refund or credit, PayPal generally continues to collect the agreed installments. Always check the fare rules and cancellation policy with the travel provider before confirming a Pay Later purchase.

Q6. Is PayPal Pay Later safer than using a credit card for travel?

It is not automatically safer or riskier, just different. Traditional credit cards often come with robust travel protections and well‑established dispute processes. PayPal Pay Later can offer similar rights in many cases, but disputes may be more complex because you have an extra party involved. The better option depends on your spending habits, your ability to pay in full and the protections offered by your specific card.

Q7. Can I pay off my PayPal Pay Later travel purchase early?

Yes. You can usually make additional payments or pay off the entire remaining balance early through your PayPal account without a prepayment penalty. This can be a smart move if your cash flow improves after booking and you want to reduce the risk of missed installments.

Q8. What if I am traveling when my Pay Later installments are due?

Installments are charged automatically on scheduled dates, whether you are at home or abroad. Before you depart, confirm that your linked bank account or card will have enough funds on those dates, and consider setting alerts so you are not surprised by debits while dealing with foreign transaction fees and on‑trip expenses.

Q9. Can I use PayPal Pay Later for vacation rentals or tours on booking platforms?

Often yes, as long as the platform supports PayPal checkout and PayPal offers Pay Later on that particular purchase. For example, some travelers use Pay in 4 for guided tours, attraction tickets or apartment rentals booked through major platforms. Always read the platform’s cancellation and refund rules, because they will govern how any changes affect your Pay Later plan.

Q10. How can I decide if PayPal Pay Later is a good idea for my trip?

Ask yourself whether you could reasonably pay for the booking in full within the next few weeks or months without strain. Map out the exact dates and amounts of each installment, consider your other debts and your on‑trip budget, and compare Pay Later to alternatives like saving longer or using a rewards credit card paid off in full. If the plan only works by assuming everything will go perfectly, it may be too risky for your situation.