Before you lock in flights, hotels, or that long-awaited cruise using Zip or a Zip-branded travel agency, it pays to understand exactly how the pricing works. Between “pay in 4” offers, planning fees, package discounts, and fine-print charges, it can be hard to tell what you are really paying for a trip. This guide breaks down how Zip-style travel financing and Zip Travel agencies charge for their services, with clear examples so you can compare options and avoid costly surprises.

Get the latest updates straight to your inbox!

What “Zip Travel” Actually Means When You Are Booking

The phrase “Zip travel” can refer to two different things that affect pricing. First, there is Zip, the buy now, pay later provider that lets you split purchases into four installments over six weeks at major travel brands such as Expedia, Hotels.com, JetBlue, Delta, American Airlines, United, Vrbo, and Amtrak. In this case, you are booking through a mainstream travel supplier or online agency and using Zip as the payment method, similar to using a credit card in installments rather than upfront cash.

Second, there are independent travel agencies that happen to include “Zip” in their name, such as Zip Travel Co or Zip Trip Travel in Colorado. These are traditional agencies that design and book trips, sometimes specializing in family vacations, Disney, cruises, or business travel. Their pricing is based on planning fees and supplier commissions rather than the pay-later structure of the Zip financing app.

Before you book, clarify whether you are dealing with a financing tool like the Zip app, a travel agency branded with “Zip,” or both. For example, you might use Zip’s pay-in-4 feature to buy a $1,200 JetBlue vacation package, while a separate Zip-named agency charges a planning fee to design a custom Hawaii itinerary. Knowing which “Zip” you are using will help you interpret what the prices and fees really cover.

In practical terms, if you see Zip offered at checkout on a site like Expedia or Agoda, you are simply choosing an installment payment method. If you are speaking with a human advisor at a Zip-branded agency, you are paying for their expertise and service, usually through a mix of visible fees and built-in commissions from hotels, cruise lines, or tour operators.

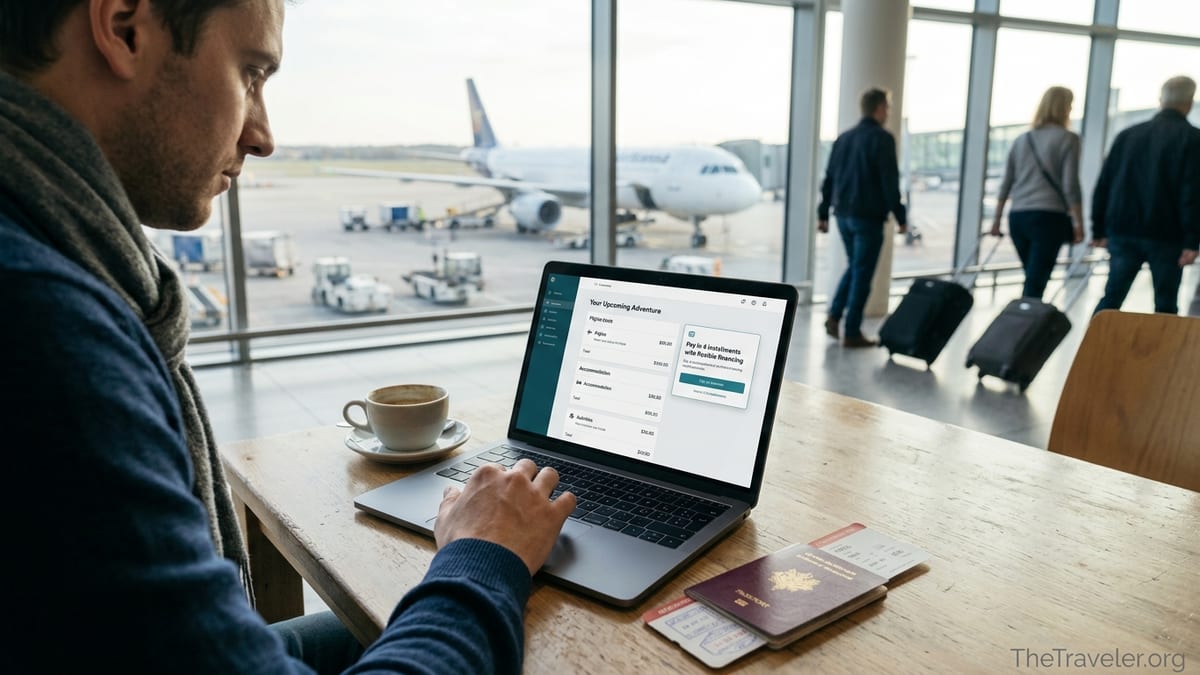

How Zip’s Pay-Later Pricing Works With Real Trip Examples

Zip’s core offer for travelers is a pay-in-4 installment plan. You make the first payment at checkout, then three equal payments over roughly six weeks. For instance, if you book a $600 hotel stay on Hotels.com through Zip’s app, you could see four payments of about $150 each, with the first due immediately and the next three every two weeks. Your room rate with Hotels.com is typically the same as paying with a credit card; you are simply spreading out when you pay.

Consider a $1,000 flight and hotel package on Expedia. At checkout, you choose Zip, which creates a one-time virtual card for the full amount. You pay $250 now, then three further payments of $250 over the following six weeks. If you align this with your paychecks, you might book a spring break vacation in January and finish paying for it by early March, even if you travel in mid-March. You can travel before the trip is fully paid off, as long as your payments stay current.

Many travelers use Zip for last-minute trips when cash flow is tight. A family might find a United fare sale with domestic flights starting under $100 one way and a three-night Orlando hotel for around $500. Total package cost reaches about $900 including taxes. Using Zip, the first payment would be about $225 at booking, instead of the full $900. The remaining installments hit every two weeks, keeping the family’s monthly budget more manageable.

The key is to look beyond the installment breakdown and check for any flat fees charged by Zip itself, potential late fees, and how the schedule lines up with your real income and bills. Even when marketing emphasizes “interest-free” pay-in-4 offers, missing a payment can trigger fees, and stacking multiple separate Zip purchases in the same month can quietly crowd out other expenses.

Fees & Fine Print You Should Watch For

When you use Zip as a payment method for travel, most of the costs are tied to your underlying booking rather than the Zip service. Airlines, hotels, and cruise lines set base fares, surcharges, and taxes. However, you still need to check for late fees, rescheduling rules, and any service fees that may apply if your payment fails or you make changes. These charges are usually modest per incident but can add up if your budget is already tight.

In contrast, when you work with a Zip-branded travel agency, their published fee schedule becomes very important. In the wider travel industry, planning fees for a simple domestic trip often fall between about 25 and 100 dollars, while complex international itineraries can run 200 to 500 dollars or more in planning fees alone. A custom two-week Europe trip with multiple cities, rail passes, and guided tours might carry a 300 dollar design fee, which could be billed before any flights or hotels are ticketed.

Some agencies charge flat research deposits or consultation fees. An advisor might ask for a 50 to 150 dollar nonrefundable consultation fee to design a honeymoon in Hawaii or a graduation trip to Paris. Another agency could bundle planning into a “concierge package,” for example a 250 dollar route-finder or custom-journey deposit that is later applied to the overall cost of the trip. While this can represent good value when you book, it becomes sunk cost if you decide not to travel or to book independently after seeing their ideas.

There are also agencies that advertise “no fees” for standard packages where they earn commission from cruise lines or all-inclusive resorts. For example, a Caribbean cruise that costs 2,000 dollars per couple may pay the agent through the cruise line, with no separate planning fee charged to you. However, if you ask that same agent to book only flights for a family of four on a busy holiday weekend, they may add a ticketing fee of 25 to 75 dollars per ticket because airlines rarely pay commission.

Real-World Pricing Scenarios With Zip & Zip Travel Agencies

Imagine you are planning a spring family vacation to Orlando from Chicago. You find a bundle on a major online agency that includes roundtrip flights, four nights at a midrange hotel near the theme parks, and airport transfers for a total of 2,400 dollars for a family of four. At checkout, you choose Zip as the payment method. Your first payment is 600 dollars, followed by three payments of 600 dollars every two weeks. There are no extra booking fees from Zip beyond potential late charges if your card fails. You are paying the standard package price, but on an installment schedule.

Now compare this with hiring a Zip-named travel agency that specializes in family trips. The advisor charges a 150 dollar planning fee to design and coordinate your Orlando vacation. They source a similar package: flights, hotel with a better pool, and airport transfers for a total of 2,350 dollars. Their planning fee is paid directly by you, and they also receive commission from the hotel and transfer provider. Your out-of-pocket cost becomes 2,500 dollars. In return, you get personalized advice, help selecting park days, and someone to call if your flight is delayed or your room is not as promised.

For many travelers, the extra 100 to 200 dollars for expert planning feels worth it for complicated trips. Consider a two-week multi-country Europe vacation: flights into London and home from Rome, Eurostar to Paris, trains to Switzerland and Italy, plus city tours and museum tickets. A specialized itinerary planning service might charge 300 to 500 dollars as a design fee on top of the 6,000 to 8,000 dollar base cost of the trip for two people. Some even provide a transparent line-by-line breakdown: 500 dollars for flights, 1,800 dollars for hotels, 700 dollars for trains, and so on, plus the planning fee.

Group travel is another area where fees surface quickly. A high school band traveling to a festival in another state might pay an initial per-person deposit, often around 25 to 100 dollars, months before departure. That deposit may be nonrefundable and separate from the agency’s commission. Further payments follow a schedule, such as 300 dollars due three months out and the balance due 45 days before travel. If the group cancels late, additional change and cancellation fees may be deducted by both the agency and the underlying suppliers like hotels and charter bus companies.

How Travel Agents Using “Zip” Names Typically Set Their Prices

Zip-branded travel agencies, like many independent agencies, generally combine three pricing elements: visible client fees, hidden supplier commissions, and occasional markups on specialized services. A family-focused agency may loudly advertise, “No fees for Disney and major cruise lines,” because Disney resorts and cruise brands already build agent commissions into their rates. In those cases, you are effectively paying for the agent’s time through the vacation price itself rather than as a separate line item.

For custom or low-commission work, most agencies rely on planning fees. A boutique advisor designing a tailored safari in Kenya or a food-focused tour of Italy might charge a 250 dollar per-trip research fee or a per-person design fee of 75 to 150 dollars, especially if there is little commission on local guesthouses or independent tour guides. Another model is hourly billing, where the agent charges 75 to 150 dollars per hour for research and booking time, capped at an agreed total.

Corporate and frequent business travelers using agencies with names like Zip Trip Travel often pay yet another way: transaction fees negotiated in a service agreement. A company might pay 25 to 35 dollars per airline ticket issued, plus service fees for after-hours assistance. The business values the ability to call a real person when flights are canceled, and in turn the agency earns a predictable per-transaction income rather than relying solely on supplier commissions.

Some agencies experiment with membership-style pricing. For example, a subscription model could charge a few hundred dollars per year and include priority response times, ongoing itinerary tweaks, and help with trip disruptions. Members might then receive discounted or waived planning fees on each individual trip. This kind of structure can make sense if you travel several times a year and want a consistent advisor who knows your preferences, airline loyalty programs, and hotel status levels.

Comparing Zip Pay-Later to Credit Cards & Other Financing

When you use Zip at checkout for travel, the main comparison is with a traditional credit card. A credit card allows you to float the entire trip cost and pay it back over months, potentially with interest, but may also offer benefits like trip delay coverage, rental car insurance, or points and miles. Zip’s pay-in-4 schedule is shorter, typically six weeks, and in many cases marketed as interest-free, assuming you pay on time. However, it generally does not bundle in the same level of travel protections that premium credit cards include.

Consider a 1,500 dollar trip to Mexico. Put on a typical rewards credit card with a 20 percent APR and repaid slowly over a year, you might pay a few hundred dollars in interest while earning points you can use later. With Zip’s four payments of 375 dollars over six weeks, there is no ongoing interest, but you must have a realistic plan to cover those larger near-term payments. For many travelers, combining a low-interest or zero-interest promotional credit card with strong travel insurance is safer for big international trips than stacking multiple short-term installment plans.

There are also dedicated travel financing options like personal loans from banks or online lenders that let you borrow, for example, 5,000 dollars for a major trip and repay it over two or three years at a fixed rate. The monthly payment could be around 150 to 250 dollars depending on the interest rate. These products are usually better suited to once-in-a-decade bucket list journeys, not routine vacations. Using Zip or similar services is more akin to spreading out a single purchase over a few paychecks.

Whichever route you choose, make sure you add in optional extras such as travel insurance, seat selection fees, baggage charges, and resort fees. A beach package that looks like 2,200 dollars might climb above 2,600 dollars once checked bags for a family of four, airport transfers, and travel insurance are added. If you are then splitting this total into four Zip payments, your installment amount could be closer to 650 to 700 dollars than the 550 dollars you expected based on the original base price alone.

The Takeaway

Whether you are using Zip’s pay-later app at a major travel site or working with a Zip-named travel agency, understanding pricing up front is the best protection against budget shocks. With Zip financing, the underlying flight, hotel, or package price is usually the same as paying in full with a card; the difference is the short-term installment schedule and possible late fees. With agencies, their value shows up in planning fees, membership models, or corporate transaction charges layered on top of supplier commissions.

Before you book, ask direct questions about planning fees, ticketing fees, cancellation terms, and how your payments are scheduled. Compare a do-it-yourself package paid via Zip to a professionally designed itinerary that includes advisory fees, and look at the entire cost, not just the monthly or biweekly number. For simple trips, using Zip to spread out payments on a standard online package might be enough. For complex international or group travel, paying a fair agency fee can actually save you money and stress by avoiding mistakes and securing better value on the ground.

Most importantly, avoid overextending yourself by stacking multiple pay-later plans or underestimating add-ons like baggage and insurance. Treat every Zip installment and every agency fee as part of one total travel budget. When you understand each component of Zip travel pricing before you click “book,” you can enjoy the trip itself with far fewer financial surprises.

FAQ

Q1. Is using Zip for travel more expensive than paying with a credit card?

In most cases, the base price of flights, hotels, or packages is the same whether you use Zip or a credit card. With Zip you spread the cost over four payments, and you may avoid long-term interest charges if you pay on time. However, you might miss out on some card benefits like robust travel insurance or rewards points, so the “cheapest” option depends on how you value those extras and whether you typically carry a card balance.

Q2. Do Zip-branded travel agencies charge extra fees on top of trip prices?

Many Zip-named agencies charge planning or consultation fees for customized itineraries, complex trips, or low-commission bookings like flights only. These can range from modest flat fees for simple trips to several hundred dollars for multi-country vacations or group travel coordination. For high-commission products such as cruises or all-inclusive resorts, some agencies waive planning fees and are paid by the supplier instead.

Q3. Can I travel before my Zip installments are fully paid?

Yes, when you use Zip pay-later at checkout with a travel provider, your trip can take place during your payment schedule. You just need to keep up with the remaining installments. Missing payments could lead to fees and may affect your ability to use similar services in the future.

Q4. What happens if I miss a Zip installment on a trip I have already taken?

If you miss a scheduled Zip payment, the service may charge a late fee and attempt to collect again from your payment method. The travel supplier has already been paid, so your flights or hotel stay will not be reversed after the fact, but failing to resolve the balance can lead to additional collection attempts and a negative impact on your ability to use Zip in the future. Check the latest Zip terms for current fee amounts and policies.

Q5. How much do travel agents typically charge for planning a vacation?

Travel agent fees vary widely, but a simple domestic trip might incur a planning fee between about 25 and 100 dollars, while a complex international or multi-stop itinerary can cost 200 to 500 dollars or more in professional fees. Some agents charge hourly rates, others use flat fees, and many rely on supplier commissions for standard cruise or resort packages, which may mean no visible fee to you for those trips.

Q6. Are “no fee” travel agencies really free?

“No fee” usually means the agency does not charge you a separate planning fee for certain trips. Instead, they are paid commission by hotels, cruise lines, or tour operators, which is built into the price you see. You are still paying for their service, just indirectly. For low-commission work like stand-alone flights or highly customized local experiences, even “no fee” agencies often add service or ticketing fees.

Q7. Should I use Zip pay-later for a large international trip?

Zip can work for medium-size purchases you can comfortably repay over six weeks, such as a short getaway or domestic flights and hotel. For a large international trip that costs several thousand dollars, a mix of savings, a low-interest credit card, or a fixed-rate personal loan might be safer. These options spread the cost over a longer period and can be paired with strong travel insurance, though you must factor in interest costs and avoid borrowing more than you can handle.

Q8. How can I tell if a planning fee is worth paying?

Ask what is included before agreeing: Will the agent handle schedule changes, monitor fare drops, or provide on-the-ground support if something goes wrong? For a straightforward three-night city break, a 300 dollar planning fee may not add much value. For a three-week, multi-country itinerary or a school group tour, a similar fee that covers dozens of bookings and contingency planning can quickly pay for itself in avoided mistakes and saved time.

Q9. Are there hidden costs in travel packages I pay for with Zip?

Travel packages may hide costs in resort fees, baggage charges, seat selection fees, airport transfers, and optional excursions. These apply whether you pay upfront or with Zip. Before you commit, check what is truly included, estimate extras for your travel style, and then calculate your total cost divided into four installments. That way you are not surprised by a higher effective payment amount once all add-ons are included.

Q10. What questions should I ask before booking any Zip travel option?

Clarify whether you are using the Zip pay-later app, a Zip-branded agency, or both. Ask about all planning, ticketing, and change fees; what happens if you cancel; how long your payment schedule runs; and whether travel insurance is included or recommended separately. With clear answers in writing, you can compare options side by side and book the one that fits your budget and risk comfort level.