Trawick International has become a go-to name for Americans shopping online for travel insurance, from semester-abroad students to retirees booking river cruises. The company’s Safe Travels series often ranks well for price and benefits, and hundreds of recent reviews describe smooth trips and fast reimbursements. Yet a steady stream of Better Business Bureau complaints and frustrated Reddit threads tell a different story: travelers who believed they were covered, only to discover that they had misread the fine print. In many of these cases, the policy itself was not the problem. The problem was how the traveler used it. If you are buying Trawick the same way you book a cheap flight, you are probably using it wrong.

Get the latest updates straight to your inbox!

The Reputation Gap: Why Trawick Feels Confusing

Trawick International sits in an unusual place in the travel insurance market. On one side, industry reviews from outlets like Forbes Advisor highlight policies such as Safe Travels Voyager for standout benefits like relatively high travel delay coverage and broad trip cancellation protection. Independent review sites in 2026 often rate the brand around 4 out of 5 stars and note a strong mix of plans for seniors, cruise passengers and international travelers. At quick glance, it looks like a safe, mainstream choice for U.S. travelers.

On the other side, consumer complaint boards and state regulator filings tell a more nuanced story. Common threads include slow claims processing, dense documentation requests, and denials tied to pre-existing conditions or missed deadlines. On ComplaintsBoard and in Better Business Bureau complaints, you see stories of travelers waiting months for decisions, or losing thousands of dollars on cruises and resort packages because they misunderstood what “covered reason” really means or filed paperwork late. The policies did, in fact, match the contract. The traveler’s expectations did not.

This gap between marketing bullet points and actual claims experience is not unique to Trawick, but the company illustrates it clearly. Many of its plans are quite comprehensive when used correctly, yet they are also strict about timing, documentation and definitions. Using Trawick well is less about hunting for an extra few dollars of baggage coverage and more about reading the effective dates, exclusions and cancellation rules line by line before you click “purchase.”

To use Trawick properly, you need to think of it as a legal contract written around specific events, not a generic money-back guarantee if anything goes wrong on your trip. Once you shift to that mindset, the patterns behind many so-called “bad experiences” become easier to understand and, more importantly, easier to avoid.

Buying Too Late: The First Big Mistake

One of the most common ways travelers misuse Trawick is by buying coverage weeks or months after they make their initial trip deposit. Many of Trawick’s trip protection plans, such as Pathway Premium, Safe Travels Voyager or Safe Travels AnyReason, explicitly tie powerful benefits to a narrow purchase window after the first payment you make on a trip. If you wait, you may still get basic coverage, but you almost certainly lose the best protections: cancel for any reason, pre-existing condition waivers, and sometimes higher medical limits.

Consider a couple in their 60s who book a $9,000 Mediterranean cruise in January through a major cruise line and only think about insurance in April, once final payment is due. They run a quick quote and buy a Trawick Safe Travels plan two days before departure. The price looks reasonable, and they see 100 percent trip cancellation for sickness. When the husband’s longstanding heart condition flares up a week before sailing and the doctor orders him not to travel, they assume they are covered. But because their policy was purchased months after the original deposit, the pre-existing medical condition exclusion was never waived. Trawick may reasonably deny the claim on contractual grounds, even though the illness is genuine.

Now contrast that with a traveler who books an $1,800 hiking tour in the Swiss Alps and purchases Pathway Premium from Trawick within about a week of paying the deposit. They insure the full nonrefundable cost and are medically able to travel on the purchase date. If they later need to cancel due to a flare-up of a previously treated knee injury, they have a much stronger case because many Trawick trip protection plans offer a pre-existing condition waiver when you buy within a specified number of days of the first deposit and insure all nonrefundable costs. The policy wording controls, but the timing of the purchase is what unlocks or closes that door.

The same timing issue affects Cancel for Any Reason coverage. Trawick’s Safe Travels AnyReason, for example, includes a Cancel for Any Reason component only when purchased very soon after the deposit and when the trip is far enough in the future. If you add the policy shortly before departure expecting to cancel for any reason at 75 percent reimbursement, you will likely be disappointed. The benefit exists only if you met the timing rules upfront.

Misunderstanding “Covered Reasons” and Cancel for Any Reason

Another way travelers misuse Trawick is by assuming that any reasonable-sounding problem counts as a “covered reason” for trip cancellation or interruption. In reality, Trawick’s policies, like those of most insurers, list specific triggers: serious illness or injury, death of a family member, weather events that close airports, a documented job loss, certain strikes and similar events. If your situation does not appear on that list or fit within its definitions, standard cancellation benefits may not apply even if your loss feels entirely unfair.

Imagine you book a $4,500 small-ship cruise in Alaska and insure it with a Safe Travels trip protection plan that includes 100 percent trip cancellation. Two months later, the cruise line changes the itinerary, dropping a marquee port and replacing it with an extra sea day. You are furious and decide to cancel. Because “changed itinerary” is typically not a covered reason in most Trawick trip cancellation sections, the claim could be denied. Travelers sometimes discover this the hard way after assuming trip insurance functions like a satisfaction guarantee.

Cancel for Any Reason is designed to plug that emotional gap, but it comes with its own rules that are easy to misuse. Trawick’s AnyReason-style plans generally reimburse a portion, often around three-quarters, of prepaid nonrefundable costs if you cancel for something not otherwise covered, such as fear of traveling during a new health scare that is not yet an official travel warning. However, you must buy the coverage within a limited number of days of the initial deposit, insure all nonrefundable costs, and cancel at least a set number of hours before departure. If you cancel the day before departure because of vague safety worries but bought the plan long after paying your deposit, or quietly underinsured the trip to keep the premium low, Trawick may legitimately decline the Cancel for Any Reason claim.

A real-world pattern shows up in online reviews: travelers cancel because they simply no longer feel comfortable with their plans, file a claim under standard trip cancellation, and then feel blindsided when Trawick denies it. The mistake is not reading the difference between named covered reasons and optional Cancel for Any Reason language before assuming everything falls under the same umbrella.

Underinsuring Your Trip and Skipping Medical Details

Price sensitivity often leads travelers to underestimate or selectively insure their trip costs with Trawick. Many of the company’s plans calculate premiums based on age, trip cost and length. When travelers see the quote jump once they enter the full, nonrefundable price of a luxury safari or multi-country cruise, the temptation is to insure only a portion or to omit prepaid excursions and internal flights. That can backfire twice: it reduces your maximum payout and, with some benefits such as pre-existing condition waivers or Cancel for Any Reason, can actually disqualify you from those protections entirely.

For instance, a family books a two-week Japan itinerary for $12,000, including $9,000 in tour and hotel costs and $3,000 in prepaid bullet train passes and local experiences. To keep the premium under a certain budget, they enter only $9,000 as the insured trip cost on a Trawick Pathway plan. When a serious illness forces a cancellation, they can reasonably expect the insurer to point out that only $9,000 was insured and cap reimbursement accordingly. More subtly, if the plan required insuring all nonrefundable costs to maintain a pre-existing condition waiver or Cancel for Any Reason benefit, they may also lose those enhancements.

Then there is medical coverage. Trawick sells both trip protection plans that bundle cancellation with medical benefits and standalone travel medical plans under the Safe Travels International and Safe Travels USA brands. Many customers simply buy the cheapest policy that meets a visa or tour requirement, without reading whether the plan is primary or secondary, what the policy maximum is, and how pre-existing conditions are handled. An American digital nomad heading to Portugal might buy a low-cost Safe Travels International medical plan, visit a clinic for a flare-up of a chronic stomach issue, and then discover that ongoing or previously unstable conditions are largely excluded. In many complaints, the issue is not that Trawick refused to pay covered emergency care, but that the traveler assumed routine or chronic treatment abroad would be reimbursed.

A safer approach is to reverse the process. First, estimate your true nonrefundable costs, including flights, prepaid tours, and special tickets you cannot easily rebook. Then, choose a Trawick plan that allows you to insure that full amount if you want cancellation coverage. Separately, consider your personal health profile and destination. If you have a cardiac history and are traveling to remote Patagonia, a plan with higher emergency medical and evacuation limits, and a carefully understood pre-existing condition waiver, is more valuable than saving twenty dollars on a lower tier.

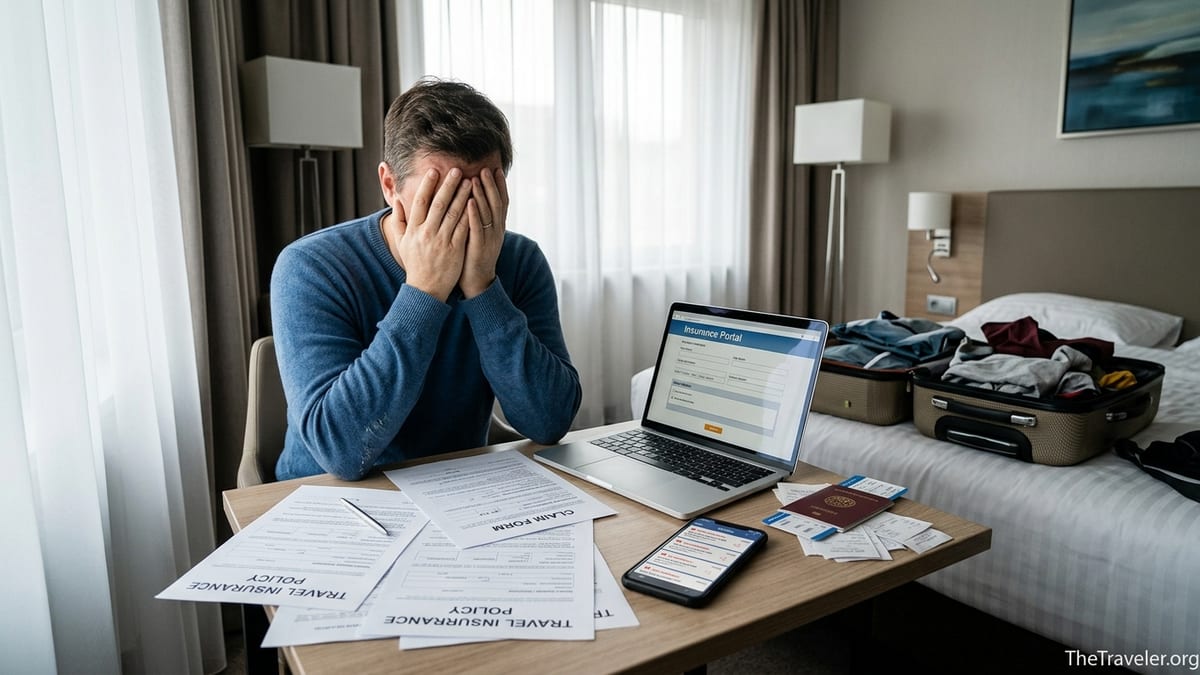

Ignoring Documentation, Deadlines and Claims Strategy

Even when travelers buy an appropriate Trawick plan, many still use it wrong at claims time. Online reviews and complaint boards often mention long claim timelines and repeated requests for documents. While some of this reflects Trawick’s own processes, a significant portion comes down to incomplete submissions and missed deadlines. Unlike airline vouchers, insurance claims rarely move quickly if you simply upload a single screenshot and hope for the best.

Consider a traveler who buys Trawick Safe Travels Voyager for a $6,000 European river cruise. A week into the trip, severe flooding forces the cruise line to cancel the downstream portion and bus guests between cities instead. The traveler decides to abandon the cruise mid-trip, books their own hotels and trains, and files a trip interruption claim with Trawick. If they submit only their new hotel receipts without proof from the cruise operator that services were disrupted or what refunds were offered, Trawick’s third-party claims administrator is likely to bounce the claim back for more information. Each back-and-forth adds days or weeks, and in some cases, missing documents within a specified time frame can lead to outright denial.

Numerous Trawick complaints also involve late filing. A traveler might assume they can wait until they are home and settled to file, only to find that the policy requires written notice of a loss within a relatively short number of days and full documentation within a longer period. If a parent visiting the United States on a Safe Travels USA medical plan is hospitalized in May but their adult child waits until autumn to file, the insurer may invoke late notice provisions. Some online stories describe situations where travelers only received action after escalating to state insurance regulators, a sign that they had allowed the process to stall rather than aggressively following up within the existing structure.

To use Trawick correctly at claims time, treat it like a legal and financial process from day one. As soon as a problem emerges, contact the 24/7 assistance line listed on your certificate, document the event with emails or letters from airlines, hotels or tour operators, and keep every receipt related to additional costs. When you file, follow the claim form line by line, upload legible PDFs instead of phone screenshots, and note your claim number, dates of contact, and the name of any representative you speak with. If weeks pass without meaningful progress, politely but firmly escalate within the company, and, if necessary, through your travel insurance comparison site or state insurance department rather than venting only in online reviews.

Choosing the Wrong Trawick Product for Your Trip

Trawick’s catalog is broader than many travelers realize, and picking the wrong type of plan is another way people unintentionally misuse the brand. The company sells trip cancellation packages, pure medical plans for international visitors, student insurance, and, more recently, cruise-specific products such as Safe Travels Sailway Cruise Plans. Each is built for a different kind of traveler and risk. Using a bare-bones medical plan as if it were a full-featured trip protection policy is a recipe for frustration.

Imagine a U.S. resident booking a $5,000 Caribbean cruise for a family of four. Instead of a trip cancellation plan, they buy a low-cost Safe Travels International travel medical policy because it appears first in the search results and boasts high emergency medical maximums. When a child breaks an arm the day before departure and the family cannot travel, they discover that their chosen plan either has no trip cancellation benefit or only a very limited interruption feature. The policy did exactly what it promised on the medical side but was never designed to reimburse nonrefundable cruise fares for a pre-departure injury.

Similarly, Trawick’s cruise-focused Sailway plans, introduced in 2026, are tuned for cruise-specific problems. They are more likely to address missed connections, port changes or shipboard medical incidents in ways that align with cruise line realities. A traveler who buys a generic trip protection plan from Trawick for a complex back-to-back cruise itinerary might still be covered for major issues, but they may miss cruise-tailored perks or higher limits on the kinds of disruptions cruises commonly face. Using generic coverage when a specialized option exists is not necessarily “wrong,” but it is often suboptimal, especially for expensive or intricate sailings.

The practical fix is straightforward: decide what you actually need covered before you shop. If your primary worry is losing nonrefundable deposits, focus on Trawick’s trip cancellation plans and ignore standalone medical options. If you are hosting elderly parents from overseas, look instead at inbound Safe Travels USA medical policies that emphasize hospital and doctor coverage, not trip cost. For big cruises, search specifically for Trawick’s cruise-labeled products. Matching the policy family to your dominant risk is one of the clearest ways to use the brand effectively.

The Takeaway

Used thoughtfully, Trawick International can be a solid part of your travel risk toolkit. Many of its policies offer competitive coverage for trip cancellation, medical emergencies and travel delays at prices that compare well with peers. Where travelers run into trouble is not usually with obscure legal fine print, but with basic missteps: buying too late after the first deposit, underinsuring the trip, assuming any problem is a “covered reason,” skipping Cancel for Any Reason when their biggest fear is simply changing their mind, or dropping the ball on documentation and claim deadlines.

Before you buy, slow down and define your trip’s real risks: nonrefundable costs, health concerns, destination infrastructure and trip complexity. Then choose the Trawick product type that aligns with those priorities, purchase it within the specified window from your initial deposit, and insure the full nonrefundable amount if you care about pre-existing condition waivers or Cancel for Any Reason. Once covered, treat the policy like a contract. Save your certificate, read the definitions of key terms such as “pre-existing condition” and “covered reason,” and be ready to document any loss in writing and with receipts.

No travel insurance company has a spotless record, and Trawick is no exception. But by understanding how its plans are structured and avoiding the most common mistakes, you can tilt the odds in your favor. Instead of becoming the next frustrated online reviewer, you become the traveler who paid a fair premium, understood the deal, and got reimbursed when it mattered.

FAQ

Q1. Does Trawick International cover Covid-19 related cancellations and medical treatment?

Coverage for Covid-19 depends on the specific Trawick plan and when you purchased it. Many recent trip protection and medical policies treat Covid-19 like any other covered illness for emergency medical care and, if diagnosed by a doctor, for trip cancellation or interruption. However, general fear of Covid-19 or travel advisories alone are usually not covered reasons for cancellation unless you have a Cancel for Any Reason benefit and meet its conditions.

Q2. How soon after booking my trip should I buy Trawick to get pre-existing condition coverage?

Most Trawick trip protection plans that offer a waiver for pre-existing conditions require you to purchase within a limited window after your initial trip deposit and to insure all nonrefundable costs. The exact number of days varies by plan and state, but it is often around two to three weeks. Buying later may still give you basic coverage, but incidents tied to pre-existing conditions are more likely to be excluded.

Q3. What is the difference between Trawick’s trip protection and travel medical plans?

Trip protection plans bundle trip cancellation, trip interruption, travel delay, baggage coverage and emergency medical benefits, and are designed for travelers with significant nonrefundable costs. Travel medical plans focus primarily on paying for hospital and doctor bills abroad and sometimes evacuation, with little or no trip cost protection. If your main worry is losing prepaid tours or cruises, you likely need trip protection. If your main concern is medical bills while already overseas, a travel medical plan may be more appropriate.

Q4. If I cancel my trip because I feel unsafe, will Trawick reimburse me?

Feeling unsafe or uncomfortable, without a specific covered event such as a documented terrorist incident or official evacuation order, is generally not a covered reason for trip cancellation under standard Trawick policies. To be reimbursed in that situation, you would usually need a Cancel for Any Reason benefit that you purchased within the plan’s required timeframe, insured for the full trip cost, and used within the policy’s advance notice rules.

Q5. How detailed does my documentation need to be when I file a Trawick claim?

Your documentation should be as complete and organized as possible. Plan to include confirmation of trip payments, invoices showing nonrefundable amounts, official notices from airlines or tour operators about delays or cancellations, medical records if an illness or injury is involved, and receipts for any additional expenses you want reimbursed. Submitting a clear, well-documented claim from the start usually leads to faster decisions and fewer follow-up requests.

Q6. Are Trawick policies primary or secondary medical coverage?

It depends on the specific plan. Some of Trawick’s trip protection and travel medical policies offer primary medical coverage, which means they pay eligible expenses first without requiring you to go through your home health insurance. Others are secondary and coordinate with your existing coverage. The schedule of benefits in your quote and certificate will spell this out, so it is important to check that detail before you buy.

Q7. Can I adjust my insured trip cost with Trawick after I add flights or tours?

In many cases you can increase your insured trip cost after purchase if you add prepaid, nonrefundable components like flights or special excursions. However, changing the insured amount later may affect eligibility for certain time-sensitive benefits such as pre-existing condition waivers or Cancel for Any Reason, which are typically tied to the original purchase window and initial trip cost. It is best to contact Trawick or your broker promptly whenever your trip cost changes.

Q8. How long does Trawick usually take to process claims?

Processing time varies with claim complexity, volume and how complete your documentation is. Some travelers report straightforward claims being resolved within a few weeks, while more complicated cases involving medical records or large nonrefundable packages can take longer, especially if additional documents are needed. Following up regularly, responding quickly to any requests and keeping records of all communications can help keep your claim moving.

Q9. Are Trawick plans good for cruises, or should I buy from the cruise line?

Trawick offers both general trip protection plans and cruise-specific products designed for sea travel. These can compare favorably with cruise line insurance, often with broader medical benefits or more flexible coverage if the cruise company itself runs into trouble. However, some travelers prefer the simplicity of buying coverage directly from the cruise line, even if benefits are narrower. The best choice depends on how much customization and independent protection you want.

Q10. What should I do if I believe Trawick wrongly denied my claim?

If you think a denial conflicts with your policy language, first request a detailed explanation in writing and compare it carefully with your certificate, especially definitions and exclusions. You can submit additional documentation or a written appeal if you believe key information was overlooked. If you still feel the decision is unreasonable, consider contacting your state’s department of insurance or the comparison site through which you purchased the policy, as they sometimes help mediate disputes.