More news on this day

Europe’s busiest summer for tourism since the pandemic is unfolding against a mounting aviation squeeze, as major markets including Germany, the United Kingdom, France, Spain and Greece juggle record demand with jet fuel constraints, trimmed schedules and persistently higher ticket prices.

Get the latest news straight to your inbox!

Record Passenger Demand Meets Constrained Capacity

Industry data and tourism surveys indicate that summer 2026 is set to be another record-breaking season for European travel, with both intra-European and transatlantic bookings remaining strong. The European Travel Commission’s most recent monitoring report highlights sustained interest in Mediterranean destinations, with Spain, Italy, France and Greece among the most sought-after countries for summer holidays, while long-haul arrivals from North America have also risen compared with 2025.

At the same time, capacity growth across European aviation has slowed. Analysis from Eurocontrol and industry research shows that the largest airline groups have made only marginal increases to flight volumes compared with last year, and in some cases have pulled back planned expansion. Network adjustments are particularly evident on short haul and secondary routes, where carriers are consolidating operations and prioritising aircraft and crews on core, high-margin corridors.

This imbalance between demand and supply is contributing to higher fares and tighter seat availability, especially on peak dates in July and August. Travel trade coverage notes that average ticket prices on many intra-European routes are up by double digits year on year, reflecting continued cost pressures and a deliberate focus on yield over pure volume.

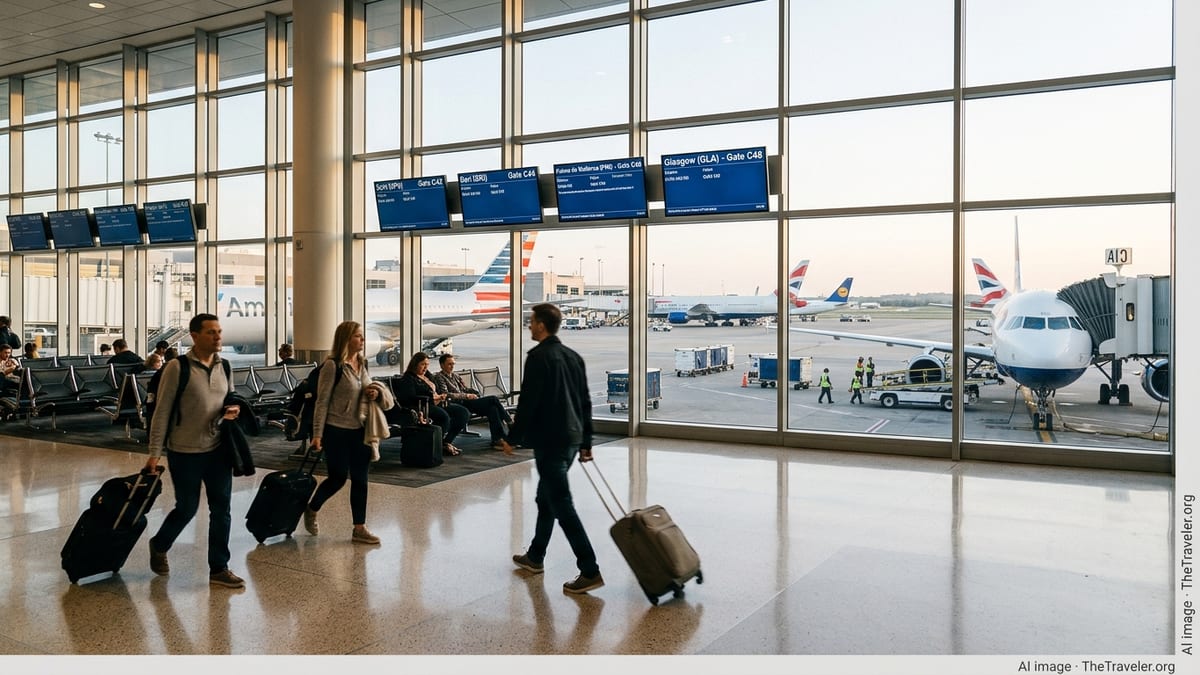

The result is that hubs such as London, Paris, Frankfurt, Madrid, Barcelona and Athens are bracing for heavy passenger flows without a commensurate increase in capacity. Airports and airlines are attempting to manage the rush through longer minimum connection times, more conservative schedules and targeted capacity cuts on less profitable links.

Germany and the UK Reshape Schedules Under Fuel and Cost Pressures

Germany and the United Kingdom, home to some of Europe’s busiest hubs, are at the centre of this structural adjustment. Aviation analysts report that leading groups based in these markets have been revising their summer 2026 timetables since late spring, trimming frequencies on thinner routes while preserving or boosting capacity on key trunk lines to North America, the Mediterranean and major European capitals.

Reports focused on Germany’s aviation market point to a cautious stance among carriers that are still managing engine supply issues and higher maintenance costs, which limit the number of aircraft that can be deployed reliably during peak season. Operational resilience considerations are prompting longer ground times and more buffer in schedules, reducing the overall number of daily rotations per aircraft compared with pre-pandemic summers.

In the UK, publicly available information shows that regulators have introduced more flexible slot management rules, making it easier for airlines to cancel or consolidate flights earlier in the season without losing valuable airport slots. Industry coverage suggests this has encouraged carriers to rationalise schedules in advance rather than risk large-scale, last-minute disruption on days with extreme weather, air traffic control constraints or fuel delivery issues.

These adjustments are intended to prevent the kind of chaotic meltdowns seen in previous summers, but they also mean fewer options for travellers and fewer spare seats when irregularities occur. Leisure passengers connecting through London or German hubs to Mediterranean and city-break destinations are being warned in consumer travel reports to expect busier flights, limited rebooking choices and higher prices when disruption hits.

France, Spain and Greece Face Heat, Crowds and Routing Disruption

France, Spain and Greece, three of Europe’s tourism powerhouses, are grappling with their own set of pressures as the peak season begins. Travel and business media describe a complex environment shaped by intense heat, airport congestion and shifting airspace patterns linked to geopolitical tensions in the Middle East and ongoing restrictions over parts of Russia.

In France, government and industry meetings earlier this year examined the risk of fuel supply constraints and potential cancellations at key airports. While national coverage has since characterised the overall risk of widespread summer cancellations as relatively low, authorities and airline managers continue to watch local supply conditions and air traffic control staffing levels, especially around Paris and major regional gateways.

Spain and Greece are contending with particularly heavy tourism flows, with data from European tourism bodies highlighting strong demand for beach destinations and island travel. Greek aviation is under additional strain from rerouting around Middle Eastern airspace, which lengthens flight times, complicates crew scheduling and increases fuel burn on services to and from the Eastern Mediterranean.

Travel reports from Greece and Spain also note that prolonged heatwaves and occasional storms can quickly ripple through already tight schedules, prompting short-notice delays and cancellations. Airlines serving coastal and island airports are devoting extra resources to irregular operations teams, but limited spare aircraft and busy runways restrict their ability to recover quickly on peak days.

Jet Fuel Shock Drives Ticket Prices Higher Across Europe

The underlying financial picture for airlines remains challenging, despite full planes. Recent forecasts from the International Air Transport Association outline how elevated jet fuel prices and the cost of rerouting around conflict zones are eroding margins globally, with European carriers among the hardest hit. The association’s June 2026 economic outlook estimated that fuel and geopolitical disruptions would roughly halve industry profitability compared with earlier expectations.

Economic research from European institutions and private analysts reaches similar conclusions, showing that the spike in jet fuel costs has been only partially offset by hedging strategies and efficiency gains. For many carriers operating dense intra-European networks, higher fuel bills are now feeding directly into ticket prices, particularly on leisure-heavy routes where demand has proven resilient.

The European Commission has issued guidance to airlines and airports on how to handle situations where local jet fuel shortages or safety requirements necessitate additional fuel carriage. The notice clarifies passenger rights and reminds operators that compensation rules still apply in most cancellation scenarios. It also acknowledges that genuine fuel shortages or safety mandates can qualify as extraordinary circumstances in some cases.

Consumer travel analyses note that passengers are already seeing the impact of these dynamics in higher base fares, new or increased surcharges and fewer promotional deals. Analysts suggest that last-minute bargain hunting is becoming less viable in 2026, as airlines hold firm on pricing to protect yields and to cover volatile operating costs.

Tourism Boom Continues Despite Cancellations and Higher Fares

Despite the aviation headwinds, there is little sign that travellers are abandoning their European summer plans. Surveys from tourism boards and travel companies show that many households in Germany, the UK, France, Spain and Greece continue to prioritise holidays, even as they adapt by shortening trips, shifting dates or choosing destinations with better air connectivity.

Industry commentary points out that some travellers are exploring alternatives to the most congested hubs and peak weekend departures. Regional airports with stable fuel supplies and less crowded terminals are seeing steady interest, while rail travel within countries such as Germany, France and Spain is picking up some of the spillover from high airfares.

For destinations that rely heavily on air access, such as Greece’s islands or Spain’s Balearic and Canary archipelagos, the immediate concern is less about a collapse in demand and more about the risk of reputational damage if repeated disruptions overshadow the visitor experience. Tourism bodies in these markets are working with airlines and airports on contingency planning, passenger information campaigns and schedule coordination to minimise visible chaos.

Across Europe, the emerging picture for summer 2026 is one of robust tourism volumes sitting uncomfortably alongside a fragile aviation system. Germany, the UK, France, Spain, Greece and other key markets are benefiting from the strongest travel appetite in years, but that boom is unfolding within an industry still constrained by fuel volatility, infrastructure limits and a cautious approach to capacity, leaving passengers to navigate a season of full planes, higher prices and thinner margins for error.